Refer for Details:

https://drive.google.com/drive/folders/19IEg3V008AkBwT5UGrsXCL8N6It7BGc_?usp=sharing

Refer for Details:

https://drive.google.com/drive/folders/19IEg3V008AkBwT5UGrsXCL8N6It7BGc_?usp=sharing

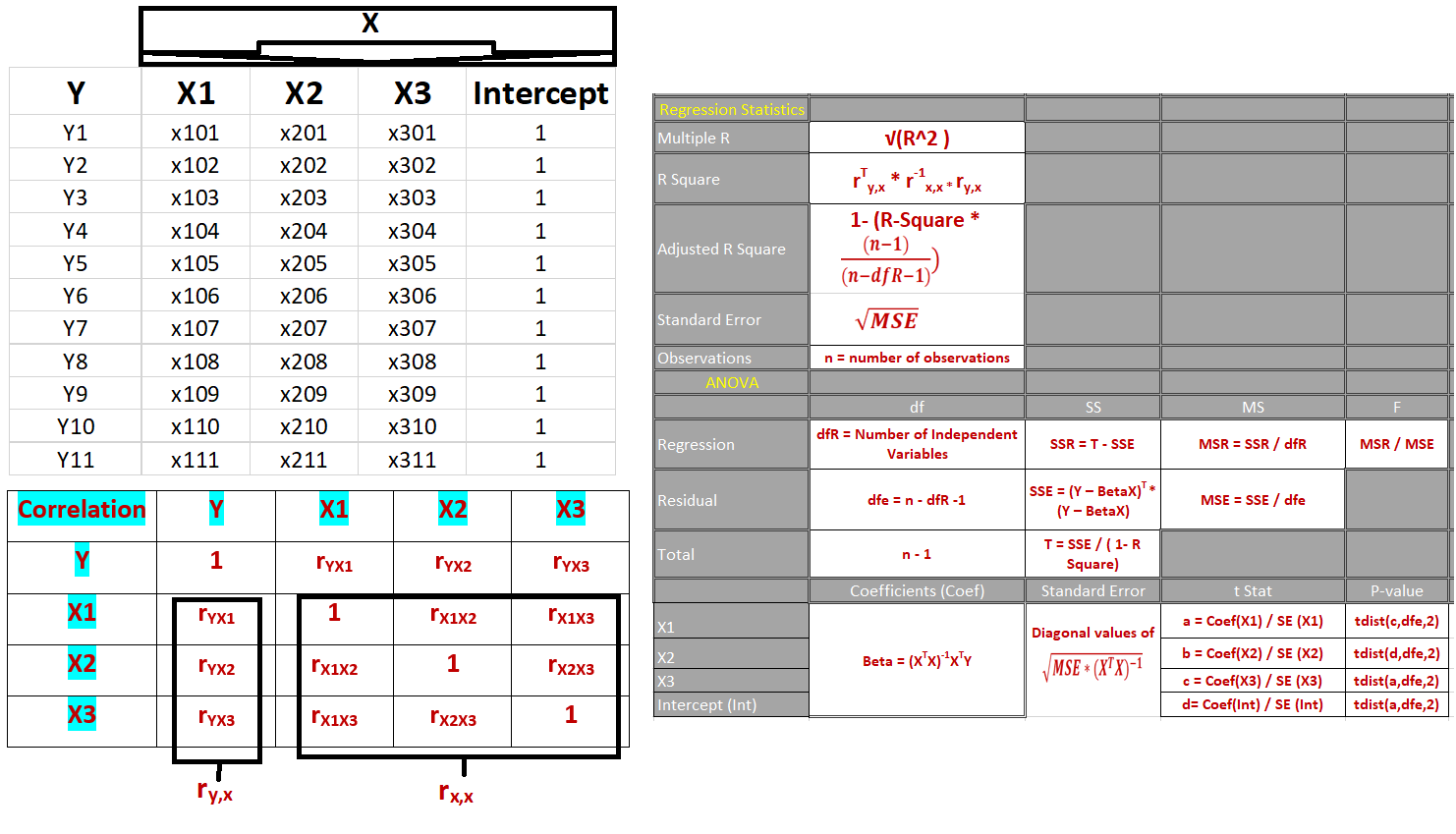

Python Generic Code (Probability of Default Model Development, Validation and Testing):

In the link below:

1- PD_Factors.csv: CSV with factors and required data

2- PD_Model_Generic_Python (Doc and PDF): Python generic code (as in steps)

3- PD_Estimate_Steps_Python: Steps in word as in Screenshot below

Errors of a model is decomposed into Noise, Bias and variance.

Bayesian Inference

Update

probability with new information (data).

Combining

two distributions (Likelihood and Prior) into Posterior.

Posterior

is used find the “best” parameters in terms of maximizing the posterior probability.

Steps:

i.

Prior: Choose a PDF to model i.e. the prior distribution P(θ).

ii.

Likelihood: Choose a PDF for P(X|θ). How the data X will

look like given the parameter θ.

iii.

Posterior: Calculate the posterior distribution P(θ|X) and

pick the θ that has the highest P(θ|X).

Calculate P(θ) & P(X|θ) for a specific θ and multiply them together. Pick the highest P(θ) * P(X|θ) among different θ’s.

Posterior becomes the new prior. Repeat step 3 as you get more data.

Beta Distribution: the probability of success on any single trial as the random variable, and the number of trials n and the total number of successes in n trials as constants.

For the Binomial Distribution the number of successes X is a random variable and the number of trials N and the probability of success p on any single trial are parameters (i.e. constants).

Key assumptions: asymptoticity, a single risk factor, and normality.

PD assumptions and violations:Modeling Low Default Portfolio Dependent Case:

VASCIEK MODEL: Dependence between the default is explained by by Vasicek model.

By using conditional probability from the Vasicek model in the case where there are no defaults, the probability of default is the solution of below equations:

Modeling Low Default Portfolio (Independent Default Events):

Pluto and Tasche method for calculating probability of default for portfolios with none or very few observations of defaults.